Unlocking Wealth: The Simple Yet Profound Cashflow Model

In our pursuit of financial freedom, the term 'wealth' often evokes images of extravagant lifestyles, endless luxuries, and stacks of cash. However, the essence of wealth boils down to a simple yet profound model known as the Cash flow Model. This ideology reframes the conventional understanding of assets and liabilities, serving as a compass guiding us toward financial prosperity.

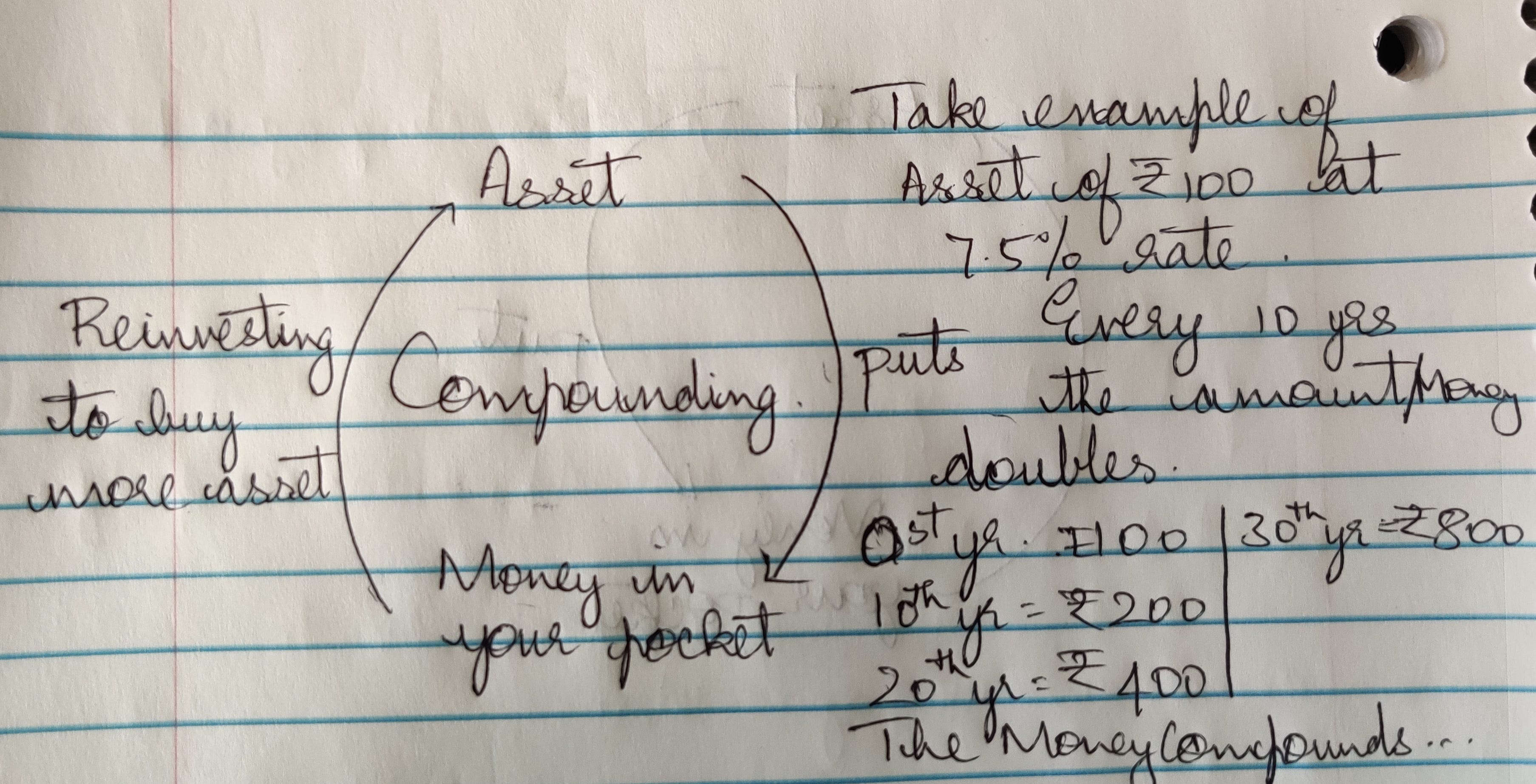

In the Cash flow Model, an asset is not merely a possession or a piece of property but a source of consistent income; it's something that 'puts money into your pocket.' Conversely, a liability is not just a debt or an obligation but anything that 'takes money out of your pocket.' The beauty of this model lies in its simplicity and effectiveness— the path to wealth is essentially a journey of accumulating more assets while minimizing liabilities.

Asset is something that puts money into your pocket.

Liability is something that takes money out of pocket.

The cornerstone of this model is intelligent investing— deploying your money to acquire more assets, which in turn, generate more income. It's a virtuous cycle of financial growth that propels you towards the coveted realm of affluence.

The trick to becoming rich is to always have more assets making money than liabilities. One way of doing this is by investing money to buy more assets.

That’s it, folks class dismissed!

Seriously, if you think about it, this is all you need to know about investing and making money.

Let me explain why.

The sign before the numbers is the rupee symbol.

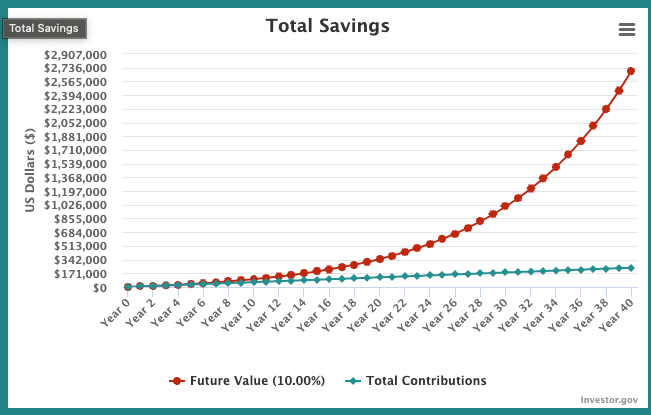

This compounding occurs when no additional money is invested. But in practice, people invest money that they earn every month. This only leads to the acceleration of wealth creation. To give you context, let’s say that your initial investment is $1000, and monthly you invest $500 at 10% return. The rate of return for the S&P 500 for the past 50 years is 10%. Could you guess how much money you would have made in 40 years? 100,000? 500,000? The results might shock you.

This is the graph for how much the money grew over time.

Food for thought:

This method also makes you question conventional assumptions like whether a house is an asset. Suppose you are using the house as a residence. It is not an asset as per the cash flow model. As each month, it takes money out of your pocket through maintenance, repairs, and other upkeeping.

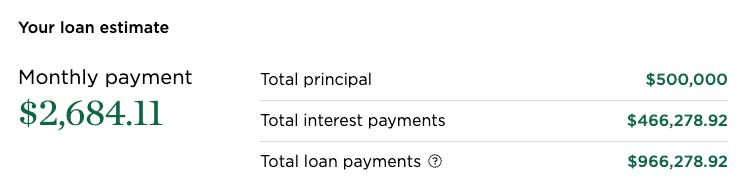

Let’s take an example to drive this point across if you buy a house that costs half a million dollars with a 30-year mortgage for a 5% interest rate which is generous as the interest rates are around 8% for homes currently. This is how much you would end up paying.

If you invest the same amount in S&P500 for the same duration at a 10% return, you would roughly make 5X more money! $5,298,023.48 to be exact. This is apart from the taxes and maintenance, which would only make the situation worse. Of course, the tax credits could always tilt the situation on either side. But the main idea is that this model gives you an intuitive understanding of how to invest.

I understand that purchasing a house is an emotional decision for many, and viewing it through monetary lenses does not capture the true reasons why many might buy homes. So I leave it up to you to decide what you should do and my dear reader, what will you do?

Credit: Most of the concepts are taken from the Rich Dad Poor Dad book.

Please share the post if you found it helpful. It encourages me to bring out bite-sized valuable content. See you in the next one!